- 27 June 2023

- By atomedya

- Bookkeeping

The unadjusted trial balance is the initial report you use to check for errors, and the adjusted trial balance includes adjustments for errors. While an unadjusted trial balance may uncover mathematical errors, the following types help in eliminating accounting errors and ensuring accurate financial statements. Check each account balance to ensure you have made all adjustments correctly and that the totals are accurate. irs announces e 2020 This step is crucial for ensuring that the financial statements prepared from this trial balance will be accurate. An adjusted trial balance is a listing of the ending balances in all accounts after adjusting entries have been prepared. Once all ledger accounts and their balances are recorded, thedebit and credit columns on the adjusted trial balance are totaledto see if the figures in each column match.

How to Prepare an Accurate Adjusted Trial Balance

If the organization is using some kind of accounting software, the bookkeeper or accountant just needs to pass the journal entries (including adjusting entries). The software automatically adjusts and updates the relevant ledger accounts and generates financial statements for the use of various stakeholders. Both the debit and credit columns are totaled at the bottom and must be equal in order to agree with the accounting equation. If the debits and credits don’t agree, there must have been an error posting the adjusting journal entries. In a manual accounting system, an unadjusted trial balance might be prepared by a bookkeeper to be certain that the general ledger has debit amounts equal to the credit amounts. After that is the case, the unadjusted trial balance is used by an accountant to indicate the necessary adjusting entries and the resulting adjusted balances.

Financial Accounting

It’s also important to consider depreciation and amortization, as these non-cash expenses must be accounted for to accurately reflect asset values. Accurate financial reporting is essential for any business, and an adjusted trial balance ensures this accuracy. By verifying that all accounts are balanced after adjustments, businesses can confidently prepare their financial statements. Bookkeepers, accountants, and small business owners use trial balances to check their accounting for errors.

When to use trial balances

Because of the adjusting entry, they will now have a balance of $720 in the adjusted trial balance. Utilities Expense and Utilities Payable did not have any balance in the unadjusted trial balance. After posting the above entries, they will now appear in the adjusted trial balance. A trial balance sheet, which in itself, is a complete summary of an organization’s transaction gives a clearer picture of it when adjusted to such expenses.

Thistrial balance is an important step in the accounting processbecause it helps identify any computational errors throughout thefirst five steps in the cycle. This step updates the individual account balances to reflect the adjustments. Ensure that the ledger balances are accurate and match the adjustments made.

Adjusting Entries

- Shaun Conrad is a Certified Public Accountant and CPA exam expert with a passion for teaching.

- Notice how we start with the unadjusted trial balance in each account and add any debits on the left and any credits on the right.

- Creating an adjusted trial balance is a critical step in ensuring that a company’s financial statements are accurate and reliable.

- An employee or customer may not immediatelysee the impact of the adjusted trial balance on his or herinvolvement with the company.

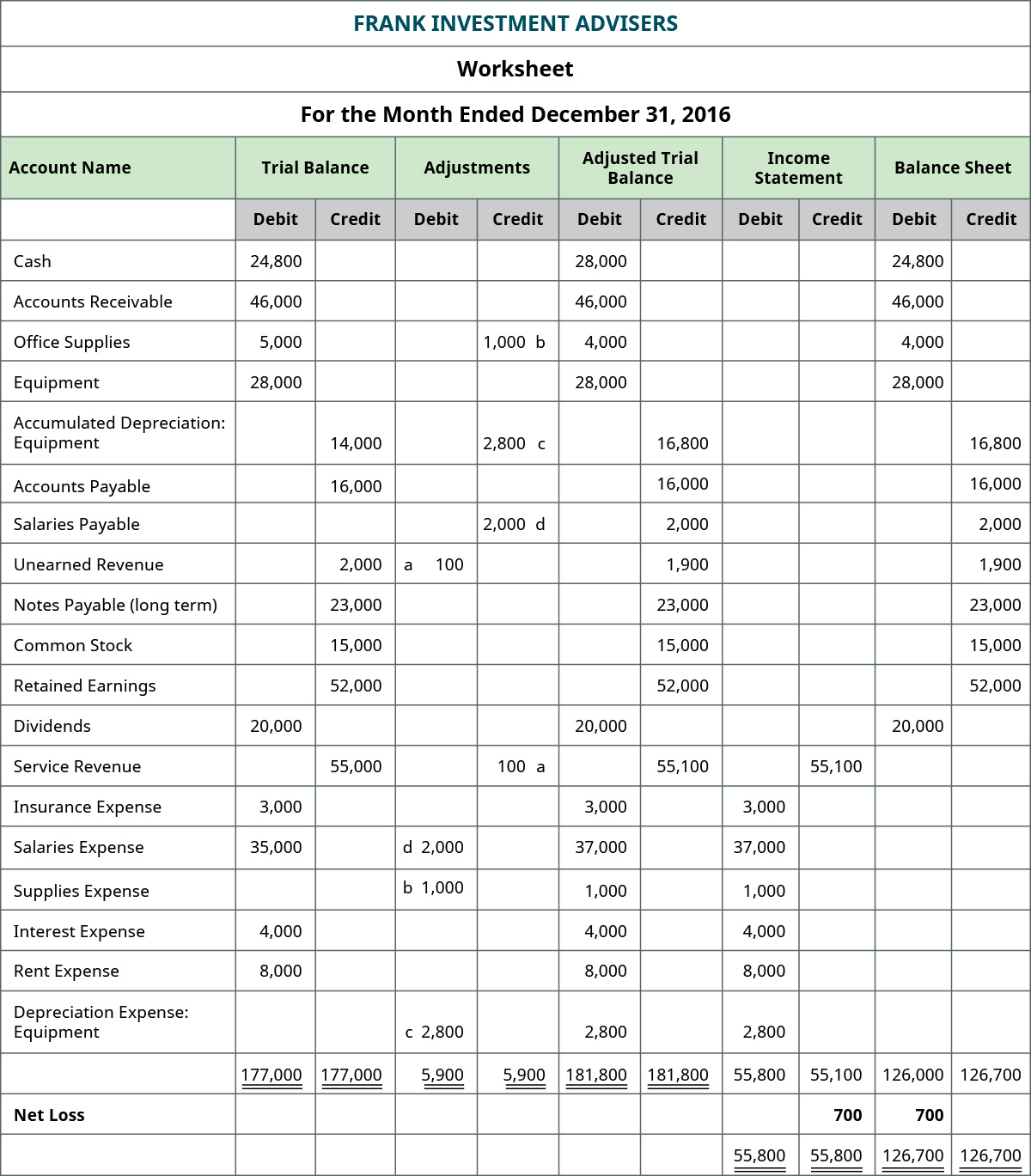

Its purpose is to ensure that the total amount of Debit Balance in the general ledger is equal to the total amount of Credit Balance in the general ledger. Adjusted trial balance records the account balances of an organization after adjusting the transaction to various expenses, including the depreciation amount, accrued expenses, payroll expenses, etc. This trial balance type allows businesses have a summarized view of all the account balances post-adjustment to respective expenditures. The adjusting entries are shown in a separate column, but in aggregate for each account; thus, it may be difficult to discern which specific journal entries impact each account. A trial balance is an accounting report you put together at the end of an accounting period to ensure the general accounting ledger is correct and the total debits match the total credits. An adjusted trial balance is formatted exactly like an unadjusted trial balance.

An adjusted trial balance lists all account balances after making adjustments. These adjustments account for accrued and deferred items, such as accrued revenues, expenses, and prepaid expenses. The primary goal of an adjusted trial balance is to ensure that all accounts are accurate and that the accounting records are ready for the preparation of financial statements. Before preparing the financial statements, an adjusted trial balance is prepared to make sure total debits still equal total credits after adjusting entries have been recorded and posted. The first method is similar to the preparation of an unadjusted trial balance. However, this time the ledger accounts are first updated and adjusted for the end-of-period adjusting entries, and then account balances are listed to prepare the adjusted trial balance.

After incorporating the $900 credit adjustment, the balance will now be $600 (debit). Hence, the trial balance includes all considerable adjustments, which is termed as adjustment trial balance. Depreciation is a non-cash expense identified to account for the deterioration of fixed assets to reflect the reduction in useful economic life. We get clear information from trial balance about debit entries and credit entries. But there is some more information required to adjust the trial balance.

This adjustment is vital for maintaining the accuracy of financial records and ensuring that all incurred costs are captured in the reporting period. Accrued revenues represent earnings that have been realized but not yet recorded in the financial statements. These revenues typically arise from services rendered or goods delivered, where payment is expected in the future.

An adjusted trial balance is a listing of all company accounts that will appear on the financial statements after year-end adjusting journal entries have been made. Before computers, a ledger was the main tool for ensuring debits and credits were equal. Along with this, the mentioned expenses relate to several accounting periods, and therefore should be distributed among them. An adjusted trial balance is prepared after adjusting entries are made and posted to the ledger. In this lesson, we will discuss what an adjusted trial balance is and illustrate how it works. When it comes to the adjustment made, the adjusted trial balance sheet is left with information that is relevant for a particular period as per the information that the business organization seeks.